Payvanta: Building a Merchant Onboarding Ecosystem

Accepting payments is not as simple as creating an account.

Before a business can start processing transactions, payment providers must collect, verify, and assess information from multiple documents, participants, and verification processes.

Payvanta helps merchants complete onboarding with confidence. This case study covers how registration and identity verification were designed as a connected sequence within a single onboarding ecosystem.

Based on real-world onboarding and compliance workflows. Some details have been modified to protect confidential information.

Accepting payments starts with verification

Two sides of the process want opposite things. Merchants want to start accepting payments quickly with as little friction as possible. Compliance teams need enough verified information to assess risk before any account can be activated.

- Fast onboarding

- Low friction

- Clear guidance

- Quick approval

- Identity verification

- Business validation

- Document verification

- Risk assessment

Without a structured process, applicants can struggle to understand requirements, and reviewers can spend significant time gathering and validating information. The result is a slower onboarding experience for everyone involved.

Who is Involved in the Onboarding Process

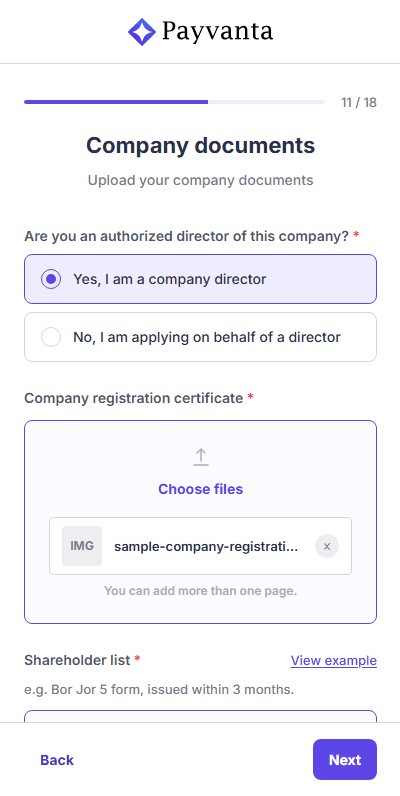

Applicants may be individuals or registered companies, and each path carries different verification requirements. For juristic entities, directors are required participants and must each complete identity verification independently before the application can proceed. See how we designed for each.

Complete onboarding quickly and understand exactly what is required to get approved.

Complete identity verification so the application can proceed.

Collect verified information to assess risk and meet AML and regulatory requirements before approving a merchant account.

What this case study covers

This case study focuses on two connected components: the merchant registration flow that collects application data, and the eKYC system that verifies identity before an account can be approved.

The application entry point

Merchants submit business details, contact information, and account preferences. This information drives all downstream verification and review processes.

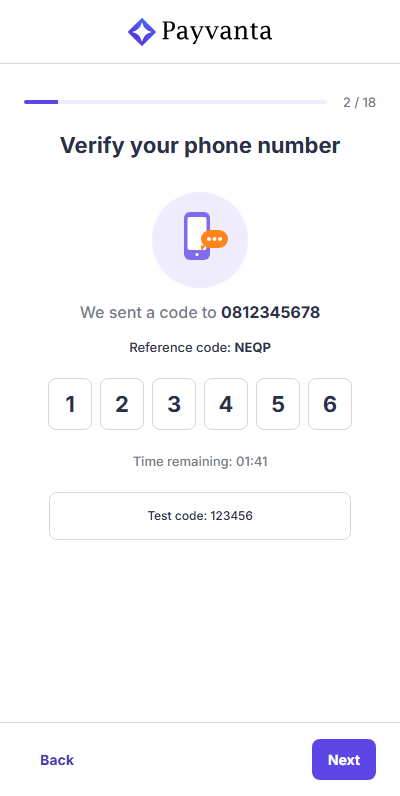

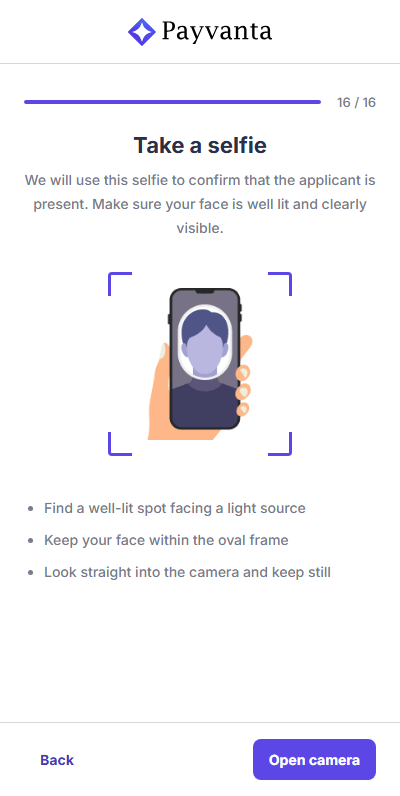

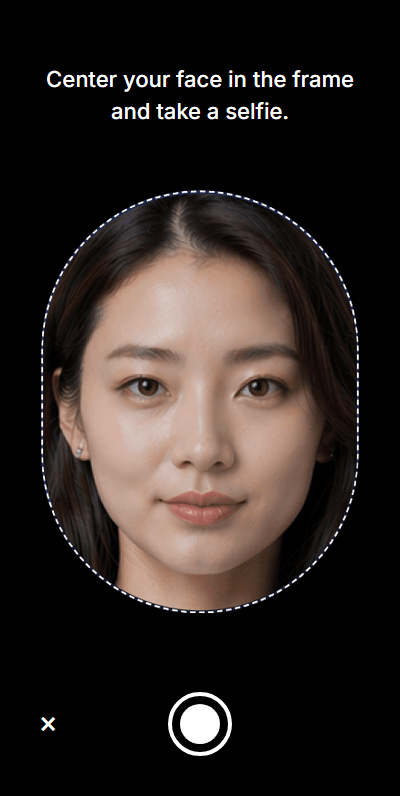

Identity verification

Applicants and directors verify their identity through ID capture and liveness checks. Results are shared with compliance reviewers as part of the approval process.

From application to approval

Both paths end at the same reviewer workspace. The key difference is that juristic entities require director identity verification before the parallel verification tracks begin.

Tested across the full registration and verification flow

Usability testing ran across 8 participants: 2 moderated, 6 unmoderated. Each session covered the full onboarding flow through to eKYC completion, with one forced fail and one pass for both ID document capture and liveness. The prototype reached 100% form completion rate, a result shaped by motivated participants and a system that had been iterated to resolve known friction before testing began.

The working prototype covers the full merchant registration flow and the director identity verification experience. Each component was designed independently but built to hand off cleanly to the next. See what testing changed →

Modules of the ecosystem

This case study covers registration and identity verification. Each module was designed independently and built to hand off cleanly to the next.